In our Weekly Market Commentary on November 17, we previewed our Outlook 2026 publication, due out on December 9. We highlighted several keys for markets next year, covering the U.S. economy, stocks, and bonds. This week, we broaden our preview and tease some other factors investors will want to consider when thinking about investing in 2026.

Quick Recap

First, here’s a summary of the keys to 2026 that we covered in our previous Outlook 2026 teaser on the U.S. economy, stocks, and bonds:

- No recession. In the absence of an economic contraction, stocks have historically delivered gains. LPL Research does not expect recession in 2026, providing a supportive backdrop for equities.

- Fiscal stimulus. The One Big Beautiful Bill Act (OBBBA) is expected to support economic growth, revenue, and profits for corporate America.

-

Solid earnings. The ongoing string of double-digit earnings growth is poised to continue. Strong earnings, bolstered by technology innovation, will be critical in supporting elevated valuations with the price-to earnings ratio (P/E) for the S&P 500 over 22 times 2026 consensus earnings per share (EPS) estimates.

-

Artificial intelligence investment and adoption. The primary artificial intelligence (AI) hyperscalers — Alphabet (GOOG/L), Amazon (AMZN), Meta (META), Microsoft (MSFT), and Oracle (ORCL) — are projected to spend $520 billion to build out AI infrastructure in 2026, potentially 30% above 2025 levels. That investment will need to fuel productivity gains for corporate America and support higher profit margins.

-

Supportive monetary policy. Federal Reserve (Fed) rate cuts aimed at normalizing policy, rather than staving off recession, would likely support further gains for stocks in 2026. If those cuts are accompanied by further progress in tamping down inflation, 2026 could be a good year for bonds as well as stocks.

-

Manageable deficit spending. If tariff revenue comes through and helps offset most, if not all, of the additional deficit spending on tap for 2026, then the yield impact of additional Treasury supply may be manageable. Stable Treasury yields should be good for stocks and bonds.

-

Stable credit markets. Despite rising idiosyncratic risks in credit markets recently, credit spreads remain tight. Healthy credit markets that help preserve those tight spreads will be key to bond market performance in 2026.

More Keys To 2026: Teaser Style

As we put the finishing touches on Outlook 2026, here are several other key factors that will drive markets in 2026 that investors will want to keep in mind.

Midterm Elections

Midterm elections in 2026 could reshape Washington and markets. All 435 House seats and one-third of the Senate are up for grabs, with Republicans holding razor-thin majorities. Historical trends suggest the president’s party often loses ground, raising the risk of a power shift. For investors, midterm years have historically been volatile, with the S&P 500 averaging a 17.5% drawdown before a typical strong rebound post-election. How markets handle this political uncertainty will be key in 2026.

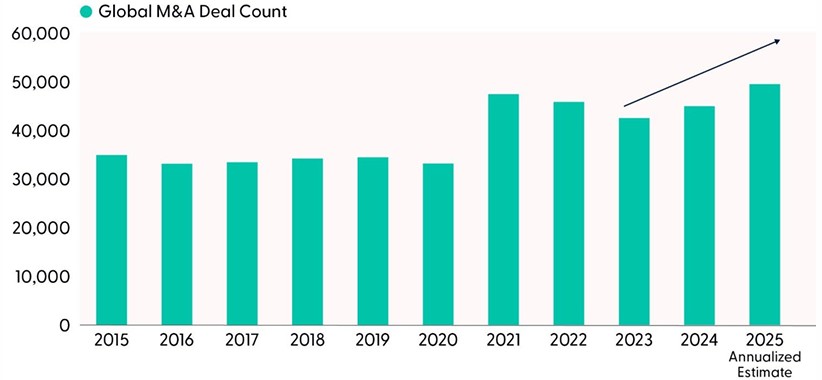

Resurgent Corporate Dealmaking

Merger and acquisition (M&A) activity is gaining traction after a muted period, driven by deregulation, Fed rate cuts, and surging demand for AI-related transactions. With deal volume trending higher, as illustrated in the “M&A Activity is Gaining Momentum” chart, it creates attractive opportunities for merger arbitrage strategies and private equity investors in the alternative investments arena. The backdrop suggests improving conditions for dealmakers, which could broaden the investible universe and support returns in 2026.

M&A Activity is Gaining Momentum

Source: LPL Research, Pitchbook 09/30/25

Disclosures: Past performance is no guarantee of future results.

Volatility, Dispersion, and Shifting Macro Conditions Shape Alternative Investments Outlook

Alternative investments may enjoy more time in the spotlight in 2026. Elevated volatility, uneven sector performance, and shifting macro conditions shape the opportunity set. Key drivers will include how strategies adapt to persistent dispersion across regions, the trajectory of interest rates, and liquidity trends in private markets. Corporate dealmaking, infrastructure resilience, and secondary offering activity could influence capital flows, while private credit faces heightened scrutiny amid rising bankruptcies. For investors, the challenge lies in identifying approaches that can navigate uncertainty and deliver returns beyond traditional stocks and bonds.

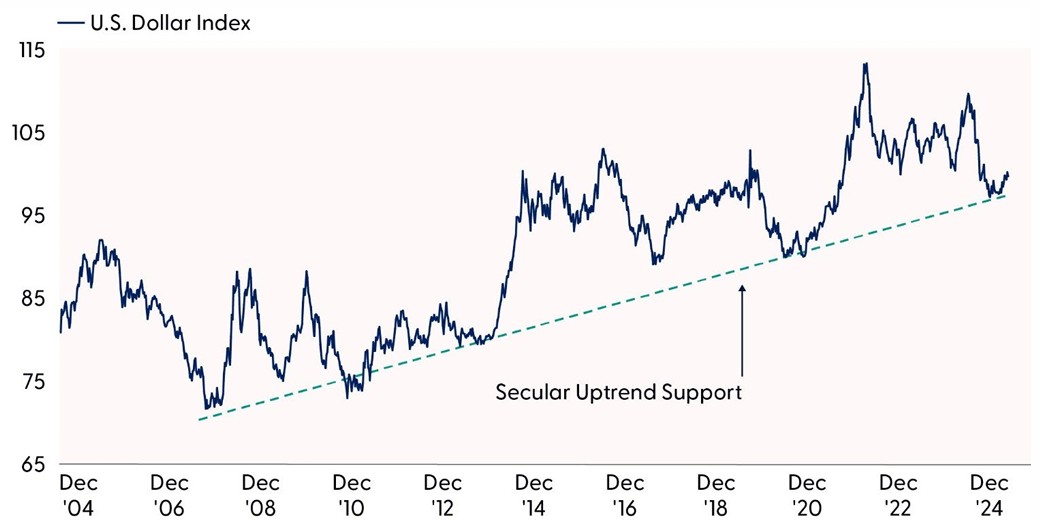

Dynamic Dollar Drivers in 2026

The U.S. dollar faced some scrutiny in 2025. Policy shocks, tariffs, and competitive pressures from Europe and China have challenged its dominance, while gold’s rising share of global reserves adds another layer of uncertainty. Key factors to watch in 2026 include trade policy direction, fiscal sustainability, central bank reserve diversification, and the dollar’s role in global liquidity. While no clear alternative exists, evolving geopolitical and macro trends will determine the greenback’s direction and influence the performance of developed international and emerging markets in 2026.

Despite sharp swings in 2025, the dollar’s decade-long rising channel remains intact. The recent pullback found support off a longer-term trend line, reinforcing the secular uptrend illustrated in the “Dollar Bulls Hold the Line” chart. A sustained break above 100.35 could confirm a short-term bottom, while a drop below 96 would signal a structural shift, potentially ending the uptrend and ushering in a bearish cycle for 2026.

Dollar Bulls Hold the Line

Source: LPL Research, Bloomberg 11/26/25

Disclosures: Past performance is no guarantee of future results. Indexes are unmanaged and cannot be invested in directly.

Cryptocurrencies May Go More Mainstream

Cryptocurrencies gained momentum in 2025 with growing institutional acceptance and deeper integration into traditional markets. Product innovation accelerated as investors explored differences among leading tokens and their potential use cases. Volatility remains a defining feature, highlighting the need for clearer regulatory frameworks. Oversight and legitimacy will be central themes in 2026 as the industry evolves.

Geopolitics as a Wildcard in 2026

Geopolitical developments will be a defining force for markets in 2026. Trade policy and evolving global alliances are reshaping supply chains, causing fluctuations in currencies and driving commodity flows. Sharp swings in copper markets this year related to tariffs underscore how policy uncertainty can spark big moves in commodities. For investors, the interplay between geopolitics, monetary policy, and global growth will determine risk premiums across asset classes.

Multiple Catalysts Ahead for Commodities

Commodities enter 2026 with multiple catalysts in play. Watch for potential Fed rate cuts and dollar weakness, which could influence metals and energy markets globally. Global growth trends — especially China’s recovery — remain critical, alongside fiscal stimulus from the OBBBA and AI-driven infrastructure investment. Industrial metals tied to electrification and green energy, plus central bank demand for gold, are areas to monitor.

As 2025 Enters the Home Stretch, Here’s Some Helpful Perspective

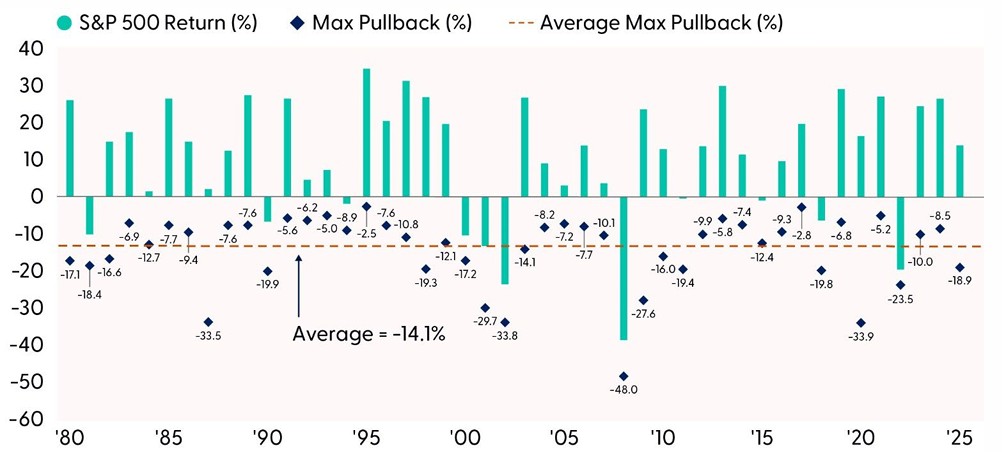

With only 23 trading days left in 2025, a strong year for stocks appears highly likely. Reflecting on the past 11 months, one element of the path stocks have followed this year that is quite common is a correction that occurred on the way to strong year-to-date gains. As you can tell in the “Another Year of Solid Gains and Large Drawdowns” chart, the S&P 500 experienced a drawdown of 18.9% this year but is still up more than 16% year to date. This pattern is not uncommon, as the chart illustrates. In fact, the average drawdown in a given calendar year has been over 14% since 1980, while the S&P 500 has gained an average of 10.7% per year during that time. Will the same pattern continue in 2026? Based on history, probably so. Keep this perspective in mind so you don’t get scared out of stocks when volatility inevitably arrives.

Another Year of Solid Gains and Large Drawdowns

Source: LPL Research, Bloomberg 11/26/25

Disclosures: Past performance is no guarantee of future results. Indexes are unmanaged and cannot be invested in directly.

Conclusion

Markets will face a complex mix of catalysts and uncertainties in 2026. Beyond the more mainstream drivers of market performance that we discussed here on November 17 (fiscal policy, earnings, interest rates, inflation, AI, etc.), midterm elections, still-evolving trade policies, and geopolitical dynamics will influence market performance in 2026. Meanwhile, corporate dealmaking in alternative investments may present opportunities, while the U.S. dollar’s trajectory remains a critical piece of the global outlook and cryptocurrency integration adds another layer to the investment landscape.

History reminds us that volatility is a normal part of the stock market, even in good years, and 2026 is unlikely to be an exception. Staying informed, flexible, and focused on key drivers will help you navigate what promises to be another dynamic year for investors. Our full Outlook 2026 will provide deeper insights into these themes — coming December 9.

Asset Allocation Insights

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains its tactical neutral stance on equities. Investors may be well served by bracing for occasional bouts of volatility given how much optimism is reflected in stock valuations, but fundamentals remain broadly supportive. Technically, the broad market’s long-term uptrend remains intact, leaving the Committee biased to buy dips that emerge between now and year-end.

STAAC’s regional preferences across the U.S., developed international, and emerging markets (EM) are aligned with benchmarks. The Committee still favors the growth style over its value counterpart, large caps over small caps, and the communication services sector. The Committee is closely watching for opportunities in the healthcare sector.

Within fixed income, the STAAC holds a neutral weight in core bonds, with a slight preference for mortgage-backed securities (MBS) over investment-grade corporates. The Committee believes the risk-reward for core bond sectors (U.S. Treasury, agency MBS, investment-grade corporates) is more attractive than plus sectors. The Committee does not believe adding duration (interest rate sensitivity) at current levels is attractive and remains neutral relative to benchmarks.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

The information presented is for educational and informational purposes only and is not intended as a recommendation or specific advice. Cryptocurrency and cryptocurrency-related products can be volatile, are highly speculative and involve significant risks including: liquidity, pricing, regulatory, cybersecurity risk, and loss of principal. A cryptocurrency fund may trade at a significant premium to Net Asset Value (NAV). Cryptocurrencies are not legal tender and are not government backed. Cryptocurrencies are non-traditional investments, resulting in a different tax treatment than currency. Federal, state or foreign governments may restrict the use and exchange of cryptocurrency. The use and exchange of cryptocurrency may also be restricted or halted permanently as regulatory developments continue, and regulations are subject to change at any time. Cryptocurrency exchanges may stop operating or permanently shut down due to fraud, technical glitches, hackers, malware, or bankruptcy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet or Bloomberg.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

For public use.

Member FINRA/SIPC.

RES-0006412-1125 Tracking #831352 | #831355 (Exp. 12/26)